Life insurance agents in the U.S. spend an estimated 40 to 60 percent of their week on tasks that do not require a license – policy data entry, renewal follow-ups, beneficiary updates, CRM management. That is time not spent advising clients or closing policies. According to a 2023 survey by LIMRA, agent productivity is the number-one operational challenge for independent life insurance agencies in the U.S.

Top Virtual Assistants for Life Insurance Agents — Quick Comparison

| VA Service | Best For | Starting Price | LI Training | Licensed VAs? | HIPAA? |

| Xassure | Life insurance agencies — all sizes | See site | ✅ LI-specific | ✅ Yes | ✅ Yes |

| Agency VA | Full-service P&C/life agencies | Custom quote | ✅ Yes | ✅ Yes | ⚠️ SOC2 |

| Cover Desk | On-demand/dedicated hybrid | Custom quote | ✅ Yes | ❌ No | ⚠️ Unclear |

| InsBOSS | Unlicensed back-office | Custom quote | ✅ Yes | ❌ No | ⚠️ Unclear |

| BruntWork | Budget-conscious agents | ~$4–$8/hr | ⚠️ General | ❌ No | ❌ No |

| Wishup | Fast onboarding | ~$10/hr | ⚠️ General | ❌ No | ❌ No |

| ℹ️ How We Evaluated These Providers We scored each provider on five criteria: life insurance-specific training depth, licensed VA availability, pricing transparency, HIPAA/data compliance certifications, and verified client reviews from insurance agents.Most providers on this list are unlicensed — meaning they cannot legally quote, bind, or advise clients on coverage. For any state-regulated activity, only licensed VAs or in-house agents can act legally. |

What a Virtual Assistant Can (and Cannot) Do for a Life Insurance Agent

The licensed vs. unlicensed distinction is the most important compliance issue you will face when hiring a VA for your agency. The NAIC’s model act on unlicensed entities is clear: unlicensed individuals can perform administrative and clerical tasks, but they cannot exercise judgment about coverage, make recommendations, or discuss specific policy options with clients.

Here is what that looks like in practice.

| ✅ Any Unlicensed VA Can Handle | 🚫 Requires a Licensed VA |

|---|---|

| Policy data entry and document filing | Discussing coverage options with a client |

| Renewal reminder emails and follow-up calls | Recommending a specific policy type |

| Beneficiary update coordination (gathering info only) | Quoting or binding a policy |

| CRM updates, scheduling, appointment reminders | Advising on coverage gaps or limits |

| Claims intake data collection and carrier follow-up | Explaining the difference between term and whole life to a prospect |

| AMS data entry, carrier portal updates | Signing any state-regulated documents on behalf of the agent |

| ⚠️ State Compliance Note Unlicensed employee rules vary by state. Some states follow the NAIC model act closely; others have additional restrictions on what a non-licensed person can say to a policyholder by phone. The National Association of Insurance Commissioners (NAIC) publishes model regulation guidance at naic.org. Review your state’s DOI guidelines before delegating any client-facing communication. |

Life Insurance-Specific Tasks Your VA Should Handle (That Most Providers Miss)

This is where the gap between a generic insurance VA and a life insurance-trained VA becomes visible.

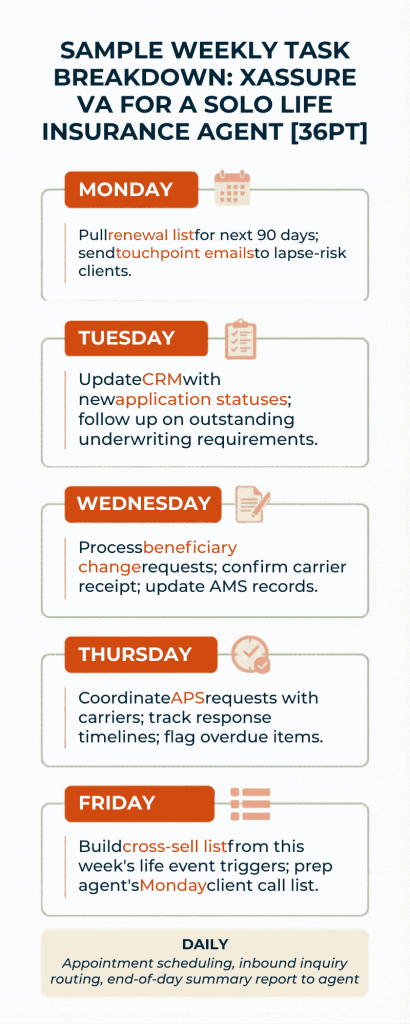

1. Term Policy Renewal Workflows

A term policy renewal is not just a calendar reminder. The touchpoint sequence needs to start 90 days out, include a rate comparison pull from the carrier, and escalate differently depending on whether the client is still in their original health class. A trained VA builds that sequence, tracks expiration dates across your book, and flags lapse-risk clients before they drop off your radar.

2. Underwriting Support

Gathering medical history documents, coordinating APS (attending physician statement) requests with carriers, and tracking outstanding underwriting requirements are full-time tasks during a busy submission period. This is detail-oriented, time-sensitive work that most generalist VAs cannot handle without extensive training. Experienced VAs know the carrier portal workflows and understand why a 30-day APS delay can hold up a policy issue.

3. Beneficiary and Policy Change Coordination

Collecting signed beneficiary change forms, confirming receipt with the carrier, and updating AMS and CRM records sounds simple. In practice it involves chasing signatures, confirming carrier-side processing, and reconciling your records when a carrier update lags. An untrained VA gets confused at step two. A trained VA closes the loop without you touching the thread.

4. Contestability Period Monitoring

Every life insurance policy issued in the U.S. carries a two-year contestability window, during which the carrier can investigate and potentially deny a death claim based on material misrepresentation in the application. Your agency should know which policies are approaching that two-year mark and not because you expect problems, but because it is relevant to how you handle coverage reviews and servicing calls.

5. Cross-Sell and Upsell List Building

Your existing policyholders are your best source of new business. A trained VA can identify clients who have had a life event like marriage, new child, home purchase and flag them for a coverage review conversation. Experienced VAs build these lists from your AMS data and CRM activity without prompting. That work rarely happens when an agent is managing their own calendar.

What Does a Virtual Assistant Cost for a Life Insurance Agent?

The honest answer is: it depends almost entirely on what you are actually buying. A $5/hr offshore generalist and a $1,500/mo insurance-trained VA are not competing products – they are different services with different risk profiles.

| VA Type | Starting Cost | HIPAA? | What You’re Actually Paying For |

| Offshore generalist (e.g., BruntWork, Wishup) | $4–$10/hr | ❌ No | Raw labor. Plan for 60+ hrs of training. Compliance risk on you. |

| Insurance-specialized retainer (InsBOSS, Cover Desk) | $1,095–$2,500+/mo | ⚠️ Unclear | Insurance admin training. But likely no licensed VA option. |

| Domestic freelance VA | $20–$30/hr | ⚠️ Varies | US-based labor. Expensive. No insurance specialization guarantee. |

| Xassure | Custom Pricing | ✅ Yes | Life insurance-trained staff. Licensed VA option. HIPAA certified. No guesswork. |

Case Study: How a Life Insurance Agent Generated $6,000 in Monthly Revenue Capacity with a Virtual Assistant

The Challenge

Many insurance agents spend a significant portion of their time handling administrative work instead of revenue-generating activities. Tasks such as:

- Policy data entry

- Renewal follow-ups

- CRM or AMS management

- Documentation and compliance tracking

While these activities are necessary, they consume valuable hours that could otherwise be spent on sales, client meetings, and relationship building.

The Solution

The agent decided to delegate administrative tasks to a trained XAssure Virtual Assistant. The VA handled routine operational work including policy processing, system updates, and renewal tracking, freeing the agent to focus on higher-value client-facing work.

The ROI Breakdown

Step 1: Determine the agent’s billable value

- Average billable/client-facing rate: $150 per hour

- This is a conservative estimate for a licensed life insurance agent.

Step 2: Measure time recovered

- Administrative workload delegated to VA: 10 hours per week

Step 3: Calculate recovered productive capacity

- Weekly value of recovered time:

10 hours × $150 = $1,500 - Monthly value of recovered time:

$1,500 × 4 weeks = $6,000

Result:

The agent regained $6,000 per month in revenue-generating capacity simply by offloading administrative work.

Human VA vs. AI Virtual Assistant — What Life Insurance Agents Need to Know in 2026

The market for insurance agency automation has changed quickly. Tools like EZLynx EVA, Strada, and Sonant AI now handle tasks that required a human assistant three years ago. That does not mean AI has replaced the human VA — it means the question has shifted from ‘should I hire a VA?’ to ‘what should a human handle versus what should a tool handle?’

When a Human VA Is Better

Complex client communication, nuanced policy research, licensed advisory tasks, and relationship-building touchpoints all require human judgment. A client calling to discuss whether to convert their term policy to whole life is not a chatbot conversation. An underwriter asking a follow-up question about a medical history detail needs a knowledgeable human on the other end. These interactions define your agency’s reputation and cannot be automated without cost.

When AI Tools Handle It Better

After-hours FAQ responses, appointment scheduling, CRM auto-population from intake forms, and routine policy status updates are well-suited to AI automation. These tasks are repetitive, rule-based, and low-stakes. Running an AI scheduling bot after hours costs a fraction of a part-time VA and handles volume that a human cannot match.

Hybrid Approach

Few agencies like Xassure, AgencyVA and CoverDesk pairs human VA expertise with AI-assisted workflows so agents get 24/7 coverage without sacrificing quality on client-facing interactions. The human handles the judgment calls; the tools handle the volume. That combination is what a solo agent or small agency needs to compete with operations that have full back-office teams.

| Use Case | Human VA | AI Tool | Best Choice |

| Complex client communication | ✅ Strong | ❌ Risky | Human VA |

| After-hours FAQ responses | ⚠️ Limited | ✅ 24/7 | AI Tool |

| Policy data entry | ✅ Accurate | ✅ Good | Either |

| Licensed advisory tasks | ✅ (licensed tier) | ❌ Never | Human VA (licensed) |

| CRM auto-population | ✅ Yes | ✅ Better | AI Tool or VA |

| Underwriting follow-up | ✅ Strong | ⚠️ Limited | Human VA |

| Appointment scheduling | ✅ Yes | ✅ Great | AI Tool |

| Relationship-building calls | ✅ Essential | ❌ Poor | Human VA |

4 Red Flags to Watch for When Hiring a Virtual Assistant for Your Life Insurance Agency

Most agents who have had a bad VA experience describe the same pattern: the hire looked fine on paper, started slow, required constant oversight, and eventually created more work than they saved. Every one of those situations traces back to one of the five warning signs below.

1. No Life Insurance-Specific Training

A general admin VA does not know what an AMS is, has never heard of a contestability period, and cannot navigate a carrier portal without a tutorial. You will spend the first two months as their teacher.

2. No Clarity on Licensing Status

If a provider cannot answer the question ‘are your VAs licensed in my state?’ with a straight yes or no, that is a compliance liability. You need to know exactly what your VA can and cannot say to a client before you give them access to your inbox.

3. No HIPAA Certification

Life insurance involves sensitive health and financial data. Any VA who touches application files, medical history records, or APS documents needs to operate under a Business Associate Agreement. If a provider does not mention HIPAA and cannot produce certification documentation, walk away.

4. Long Lock-In Contracts With No Trial Period

A provider confident in their service does not need to lock you in for six months before you have seen results. Avoid any arrangement that does not include a structured ramp-up period with defined milestones.

How to Onboard a Virtual Assistant at Your Life Insurance Agency

The agents who get the most out of a VA hire are the ones who do the preparation before day one. A VA can only replicate a process that exists on paper.

If your renewal workflow lives entirely in your head, your VA’s first 30 days will be spent figuring out what you do, not doing it.

| ✅ VA Onboarding Checklist (First 30 Days) ☐ Document your top 5 recurring admin tasks before day one ☐ Create logins for AMS/CRM with VA-specific permissions (read/edit, not admin) ☐ Set up a shared inbox or communication channel (Slack, email alias) ☐ Write a one-page standard operating procedure for each delegated task ☐ Schedule a daily 15-minute check-in for the first two weeks ☐ Identify 2-3 low-risk tasks to start with (CRM updates, scheduling, renewal reminders) ☐ Review completed tasks at end of week 1 and provide feedback ☐ Expand task scope in week 3 based on performance ☐ Confirm HIPAA compliance acknowledgment is signed before sharing client data ☐ Set 30-day milestone: VA handling at least 10 hrs/week of delegated work independently |

Why Xassure for Life Insurance Agents?

Most VA services in the insurance space were built for property and casualty agencies. They know ACORD forms and commercial lines. They do not know contestability windows, APS request workflows, or why a term policy lapse at month 23 is a different problem than a lapse at month 25. That gap matters when your VA is the one managing your policy pipeline.

Xassure was built around life insurance operations specifically. That distinction shows up in five concrete ways.

1. Life Insurance-Specific Training

A generalist VA who has worked in property and casualty will not automatically know how to track a 2-year contestability window, pull an attending physician statement from a carrier portal, or flag a whole life policy coming up on a paid-up addition review date. Xassure VAs train on these workflows before they ever touch a client file. The difference is visible in week one, not month three.

2. Licensed and Unlicensed VA Options

This is the biggest structural differentiator in the market. Every other provider on this list offers unlicensed support only. Xassure offers a licensed VA tier for agents who need help with tasks that cross into regulated activity — coverage discussions, state-filed document handling, and similar work. If your agency is growing and you need more than a data-entry assistant, that licensed option changes what you can actually delegate.

3. HIPAA-Certified Data Handling

Life insurance applications collect medical history, prescription records, and financial disclosures. That data is sensitive. If you hand it to an offshore generalist without a HIPAA business associate agreement in place, you are holding the liability when something goes wrong. Xassure’s HIPAA certification removes that risk from the table. Cheaper providers do not offer this, and most do not tell you that upfront.

| ⚠️ E&O and Data Liability Warning Sharing client health and financial data with a VA who has no HIPAA compliance framework is an E&O exposure — not just a privacy concern.If a non-HIPAA-compliant VA mishandles policy application data and a client’s protected health information is exposed, your agency can face regulatory action regardless of whether your carrier was involved.Always require a signed Business Associate Agreement (BAA) before sharing any client file with a third-party VA or staffing service. |

4. Free for 2 weeks

Almost every competitor in this space requires a discovery call before they tell you what anything costs. Xassure gives you two weeks of free service.

For an independent agent watching margin closely, that is a meaningful difference. And you cancel anytime, if you don’t like. No questions asked.

5. Fast Onboarding

The average ramp-up for a generalist VA with no insurance background is 60 to 90 days before they are operating independently. That is two to three months of your time spent training someone who still does not know your AMS. Xassure’s onboarding is designed around a 30-day milestone framework, with structured check-ins to expand task scope as competence builds. Most agents report their VA is running standard workflows in week two.

One independent life insurance agent in Texas who moved to Xassure from a generalist VA service reduced their weekly admin workload by 12 hours within the first 30 days — time that went directly back into client calls and policy reviews.

Frequently Asked Questions

No. Selling, quoting, or binding a life insurance policy requires a state-issued license. An unlicensed VA cannot legally engage in any sales activity, including discussing coverage options or recommending a specific policy. Xassure’s licensed VA tier is designed for agents who need assistance with tasks that require licensure.

You are not legally required to disclose the use of a back-office assistant for administrative tasks in most states, but your agency’s transparency standards may call for it. For client-facing communications — emails sent on your behalf, appointment reminders, document collection — it is good practice to use your agency email and your signature, regardless of who sends the message.

Xassure VAs are trained on the most widely used platforms in life insurance agency operations, including Applied Epic, EZLynx, HawkSoft, AgencyZoom, and Salesforce. If you are running a niche or proprietary system, Xassure’s onboarding team will assess compatibility before placement.

Get started in 24 hours. You also get two weeks of free service.

It is safe when the VA operates under a HIPAA-compliant framework with a signed Business Associate Agreement in place. Xassure’s HIPAA certification covers this requirement. For generalist or offshore VAs without HIPAA compliance documentation, sharing protected health information from insurance applications creates real liability. Do not do it without the paperwork in place.